Category Archives: Real Estate

Nathan Ruffing – Signature Real Estate

Licking County Parcel 095-111846-00.000: The Intel Plant

I saw 6.9 acres listed “near the Intel plant” for $5.5M and the listing basically said, “go ahead and bull-doze our house,” so I decided to investigate this thing.

The main Intel parcel where the initial buildings are planned / being built is Licking County 095-111846-00.000, click here for the Licking County auditor’s website information. The site is a ~500-acre parcel to the southwest of the intersection of Mink Street and Green Chapel Road. To get there by car, the nearest landmark you can easily navigate to currently is Kyber Run Golf Course. The Intel plant site is a 7.5 mile drive northeast from New Albany.

According to some articles, the City of New Albany will annex the plant, which sounds right because it seems like Les Wexner was involved in attracting Intel.

I believe these are some of the lucky folks who sold their farm to Intel. They got at least $13.4M I think, but hard to follow because multiple parcels got merged to put together 500 acres. The Heimerl’s still own ~75 acres across the street from the plant to the north and various other plots in the area.

Click here for Intel’s announcement.

There are various plots around the Intel plant owned by MBJ Holdings, LLC, which is explained in this WOSU article about the wetlands involved.

“MBJ Holdings LLC is a subsidiary of real estate developer New Albany Company, which was started by L Brands founder Les Wexner and Jack Kessler to develop New Albany. It submitted the application that was drafted by EHM&T engineers.”

Gone Sailing

On 2 November 2020 I decided to depart the corporate career path (energy engineer) for the rest of my life. My knee-jerk solution was to learn to sail and make sailing my occupation somehow. Regardless of what I do, I made the decision because of a fundamental idea: I am convinced that true progress in the next several decades will not be in new technologies, but in learning to use the existing technologies in a more wholesome way. As I went down the list of categories on my blog, I realized my decision affects almost every category.

Brazil Now What Migration Series: I once again do not know where I will go.

English Lessons: language is basic. Will I teach English from a sailboat?

Industrial Change Surfing: Industrial Change Surfing is about decisions – this was an enormous decision based on industrial changes.

Rage and Frenzy Politics: I believe the current polarized divisive politics partly arise from frustration with the diminishing returns of tech. (A pause for sailing is in order!)

Real Estate: boats are floating real estate. (the tax is maintenance!)

Travel: Sailing is the oldest form of long-distance water travel!

Ventures Quarterly: I have not been faithful to quarterly updates lately, but this obviously represents a ventures update.

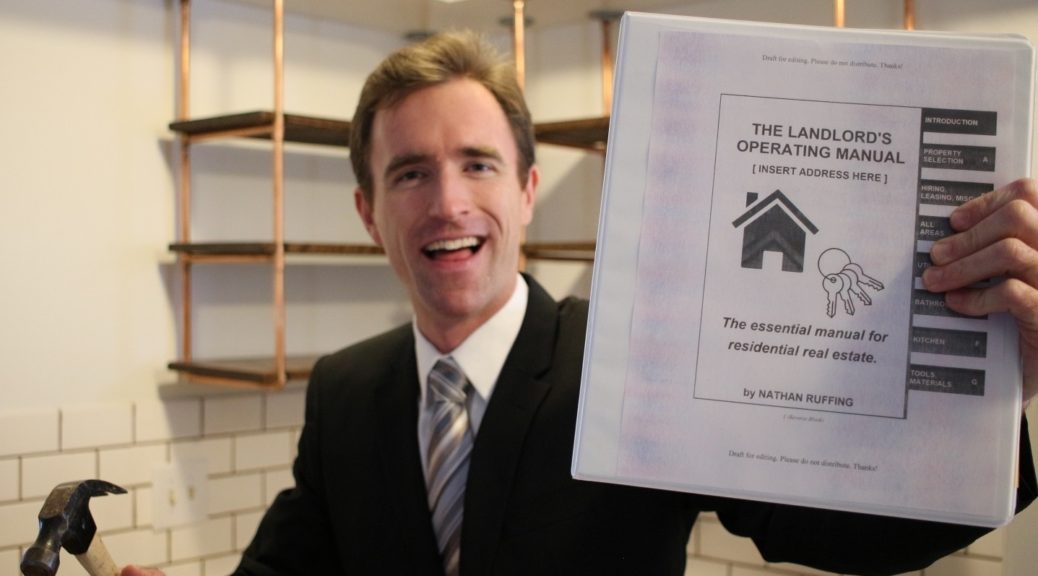

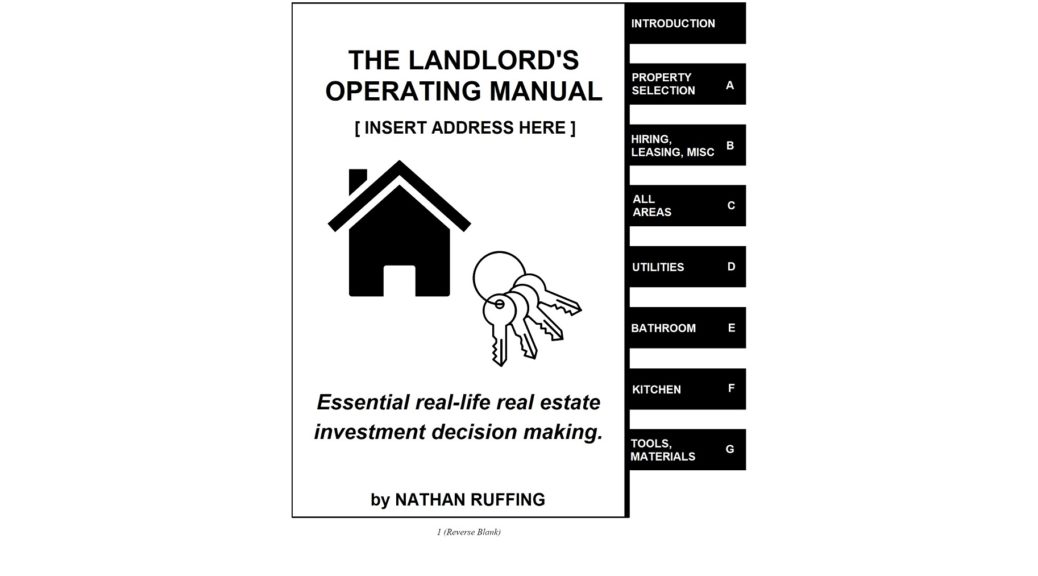

The Landlord’s Operating Manual

Introduction Video

Same introduction video on YouTube

Buy the manual here Amazon link.

I was interviewed on a [great] podcast. Check it out here.

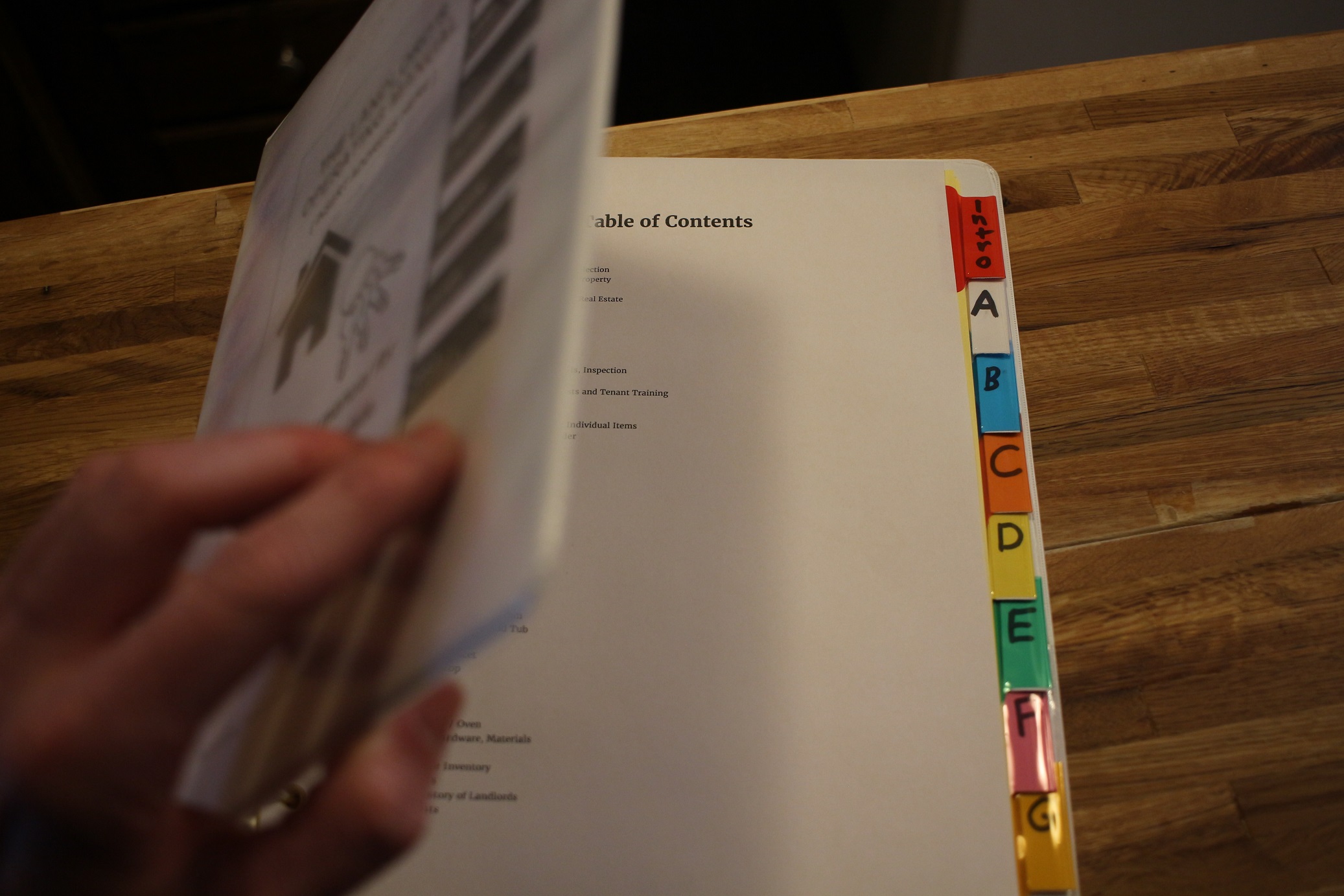

The Landlord’s Operating Manual Photos

Nate’s Real Estate Investor Tools including evaluation spreadsheet

Testimonials

This books is unlike anything else you will come across in the real estate industry. There are thousands of books written on rental properties, but none of them outlines anything further than property acquisition and first principle property management. This book is truly an operator’s manual. The author gives you an in depth view into what running a successful residential real estate operation looks like. He lays out all the plans and even details most of the mistakes he made so you do not have to. This book is ideal for anyone who is interested in owning and operating residential real estate.

The Landlord’s Operating Manual Lives on Here

I clicked the big final “publish” button on 27 January 2020. The press is set. However, The Landlord’s Operating Manual is a living document so as suggestions come in from readers I will post them right here – organized by chapter for easy reference!

A1. Guiding Principles for Selecting a Property

- Thanks to Mike Robinson of the Robinson Realtor Team (click here and call them for Central Ohio Real Estate!) for the first additive feedback. He agrees that water is critical when selecting a property but would like to have seen more about water inspection before purchasing a property. Look for grading away from the property. Look for a good sump pump and a back-up sump if possible that works in a power outage especially if the sump pump is critical to the basement being dry. Be sure your inspector gives you good details about water drainage and you pay attention to them. Categorize water issues into ones that are permanent (in a flood zone for example) and ones that could possibly be remedied (clogged downspouts for example). Can anybody suggest a link to a good detailed exterior water inspection list?

The Landlord’s Operating Manual Photos

Origin of the Manual

Helicopter Manual

The Building

Various Jobs and the Manual as Notes

Introduction

The Manual Now

Section A

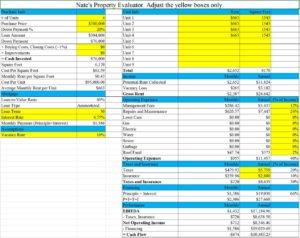

A2. Property Evaluation Spreadsheet

Section B

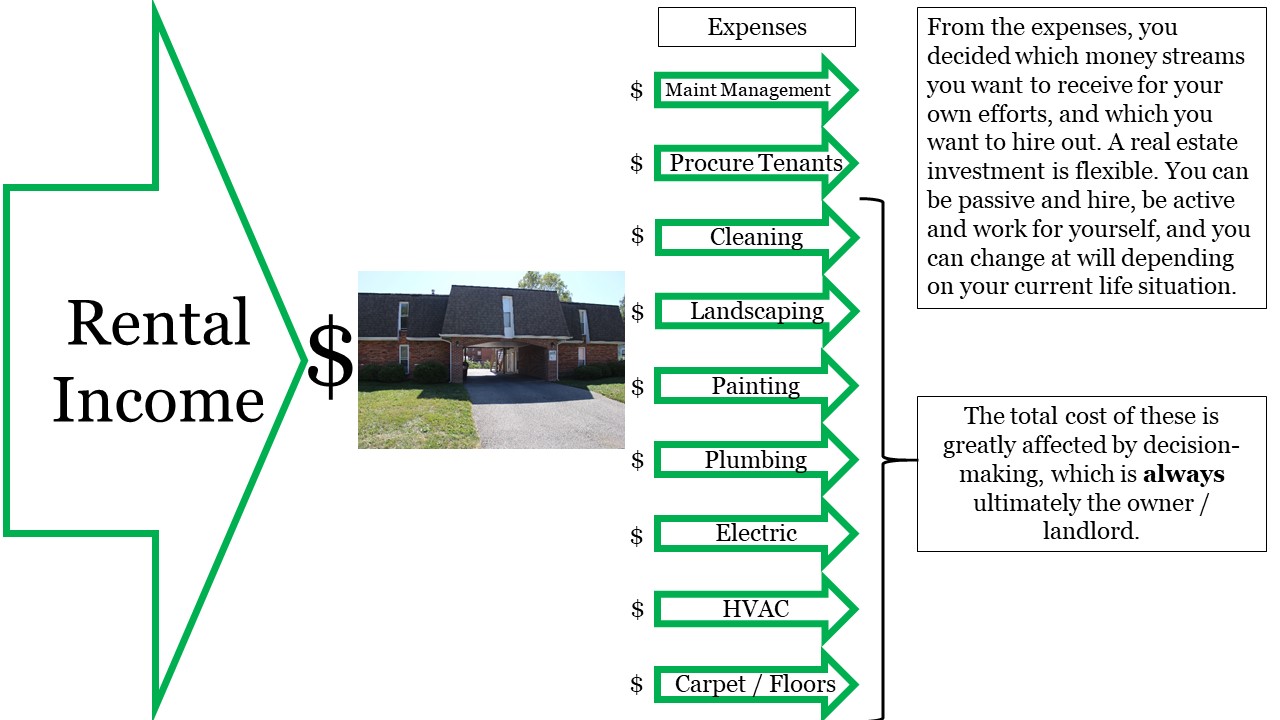

B1: The “Money Flow” Decision Chart

B5: By-Unit Spreadheet

Section C

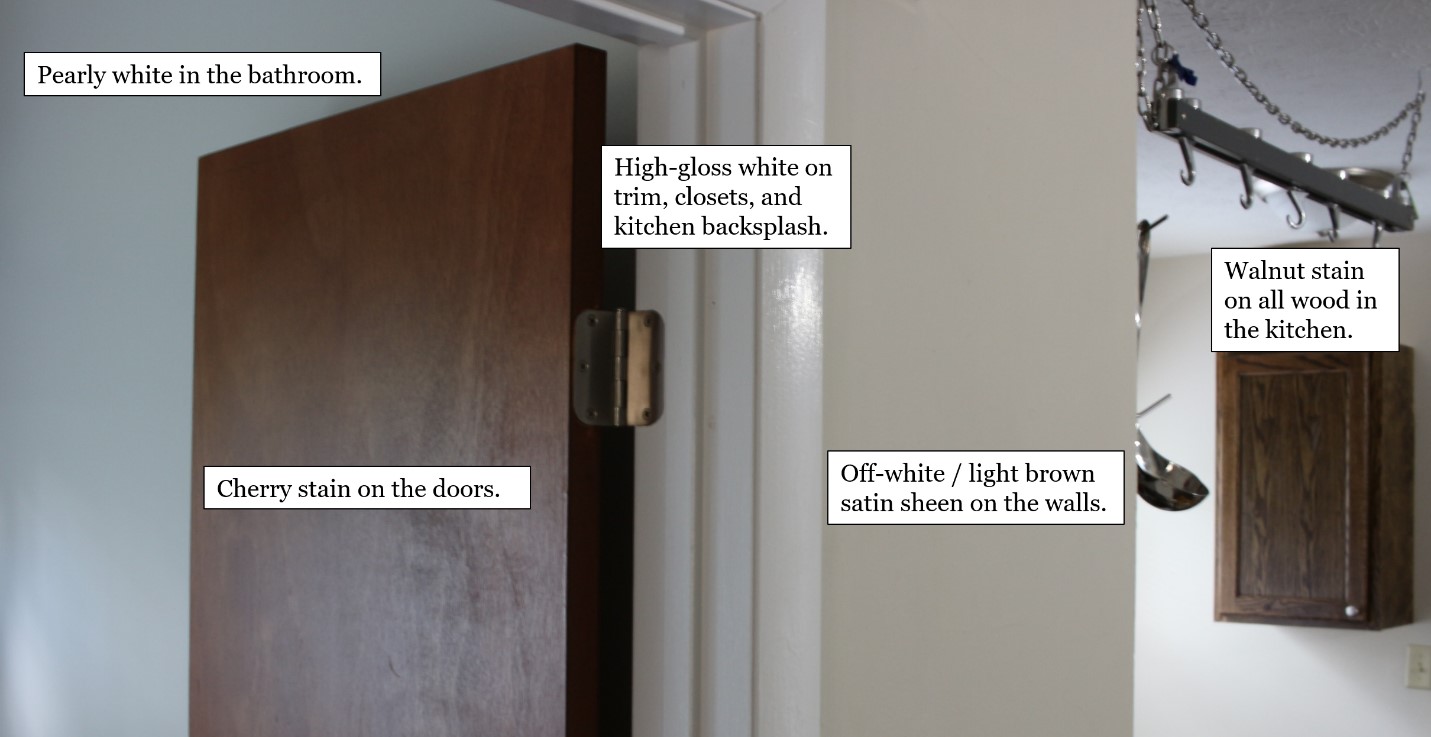

C3: Paint Colors

C3: Paint Patch Straight-On

Same Paint Patch with Glare

C3: Painting Don’ts

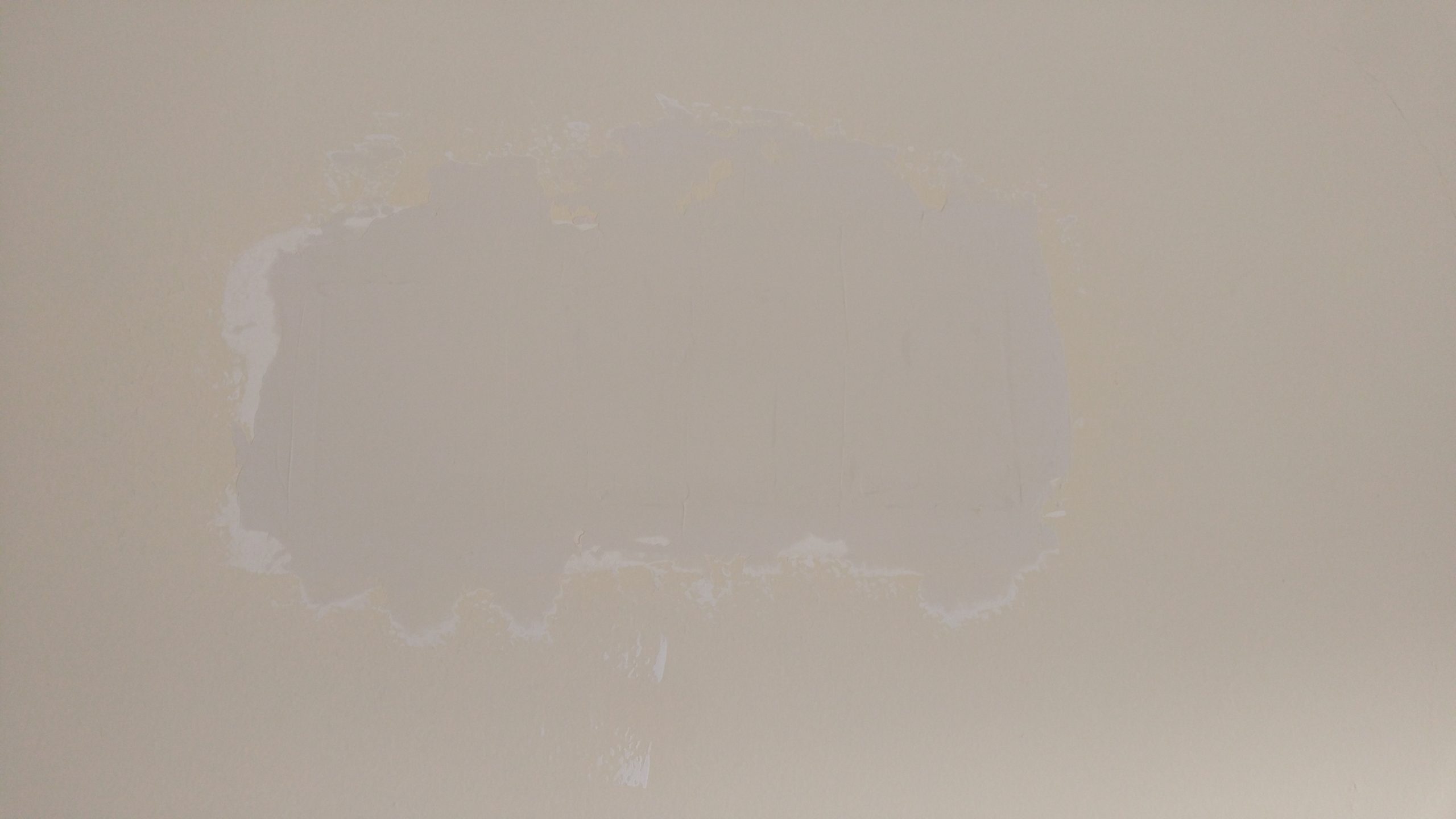

C3: The Structural Coat of Mud

C3. One Structural Coat, One Finish Coat

C3: Noxious Scum

C4: Carpet and Floor

C4: Carpet not Flooring

C5: Tub Shifted After Floor Install

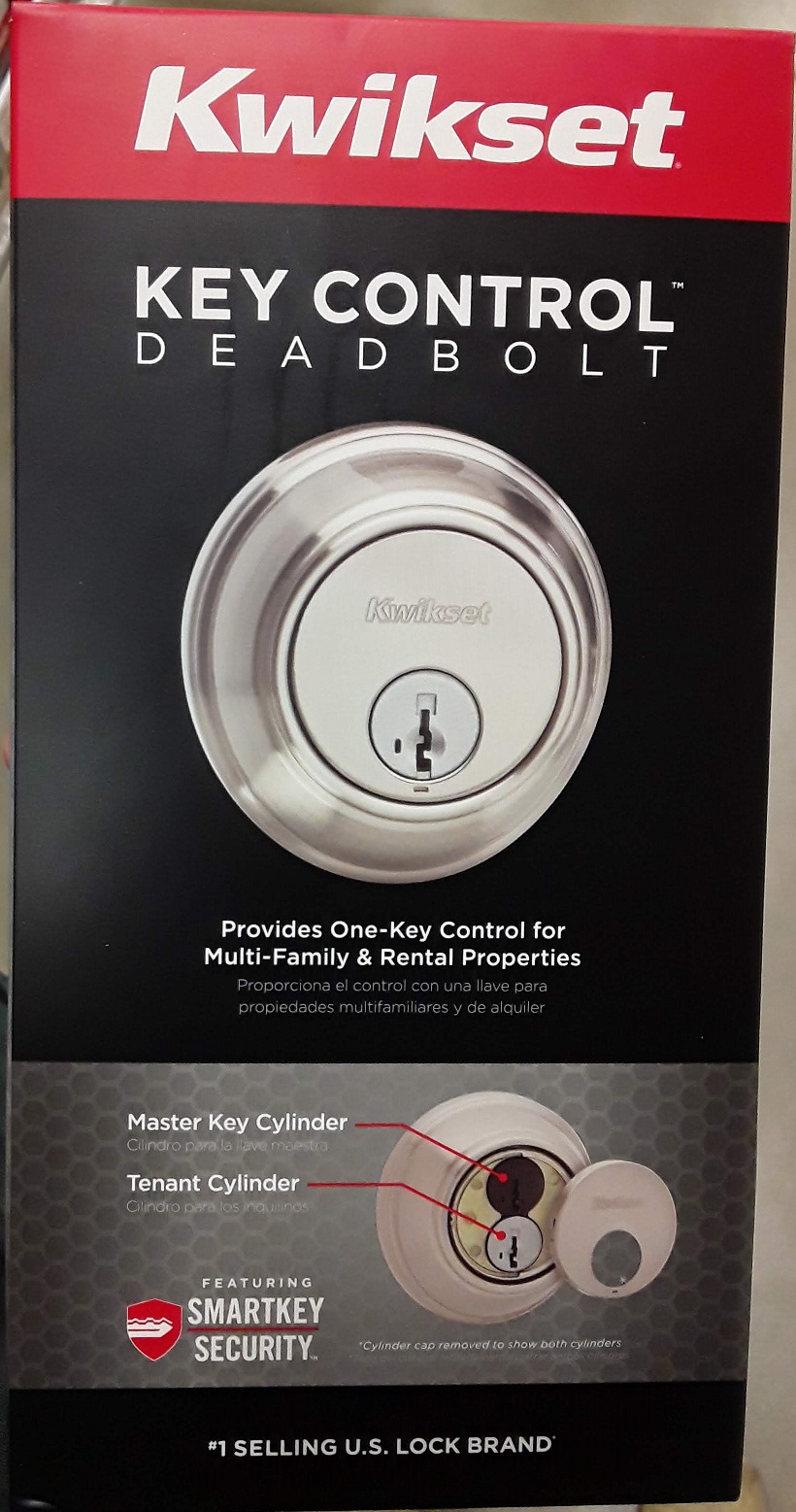

C6: Dead Bolts

C7: Boxwood Bushes!

Section D

D1: Gate versus Ball Valves

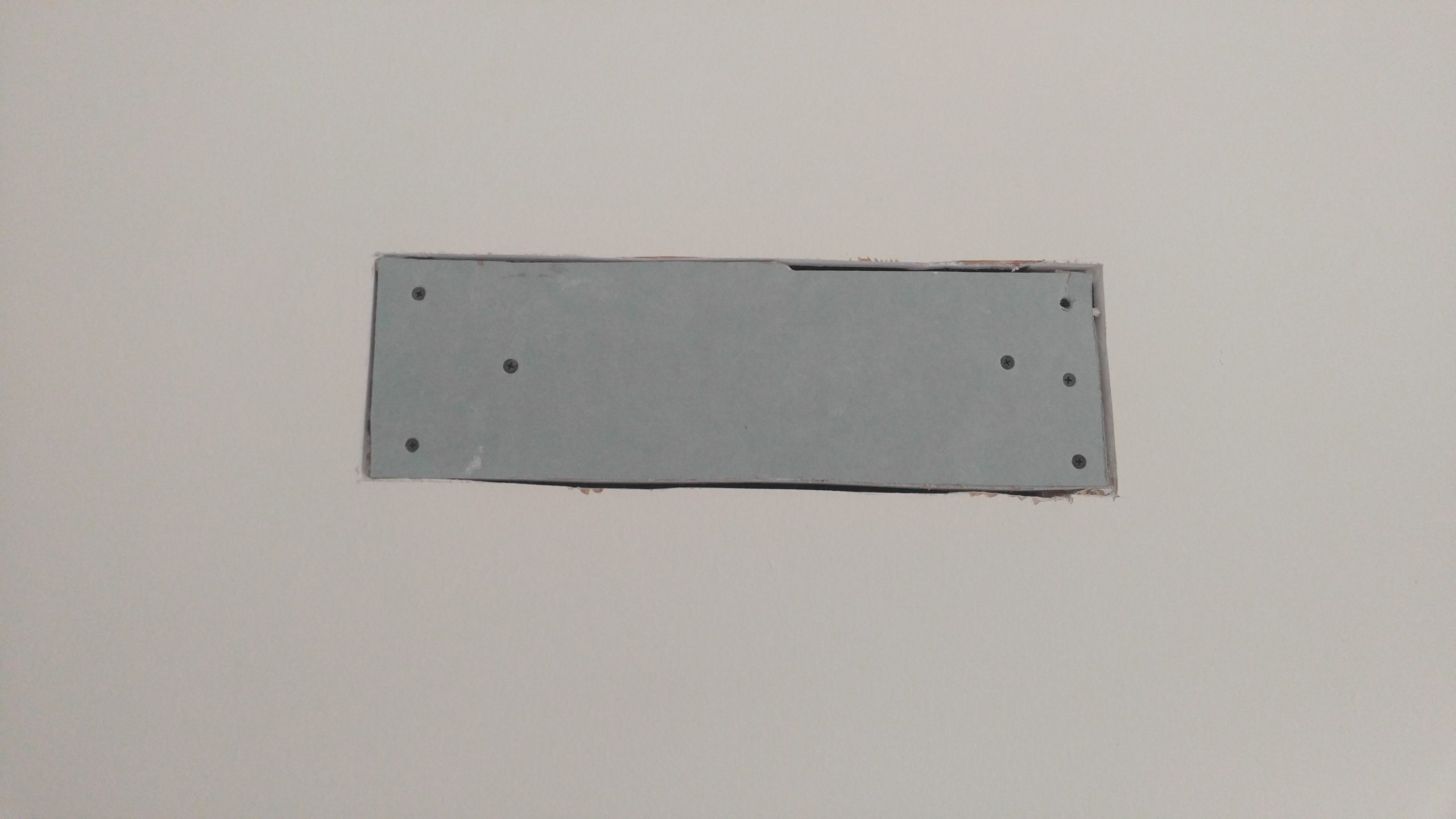

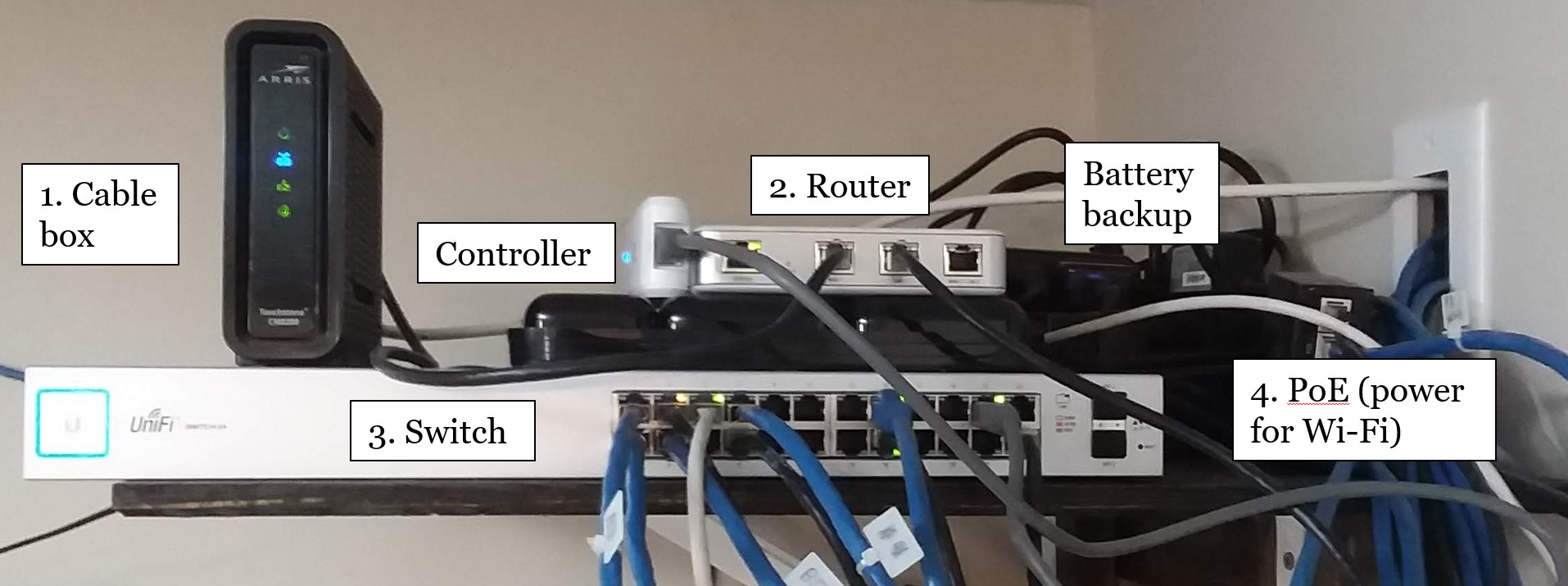

D4: Internet Equipment

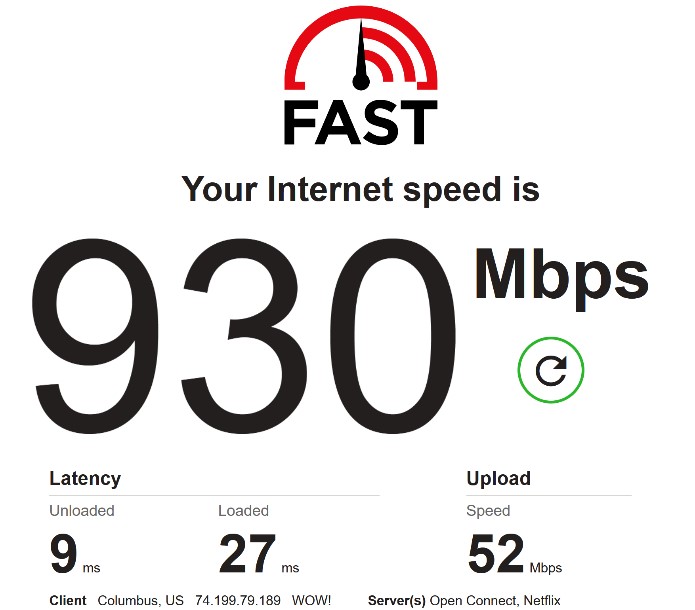

D4: Internet Speed = Fast

D4: Network Diagram

Section E

E: Hang Towel Near Shower

E1: Toilet

E1: Better than Wax

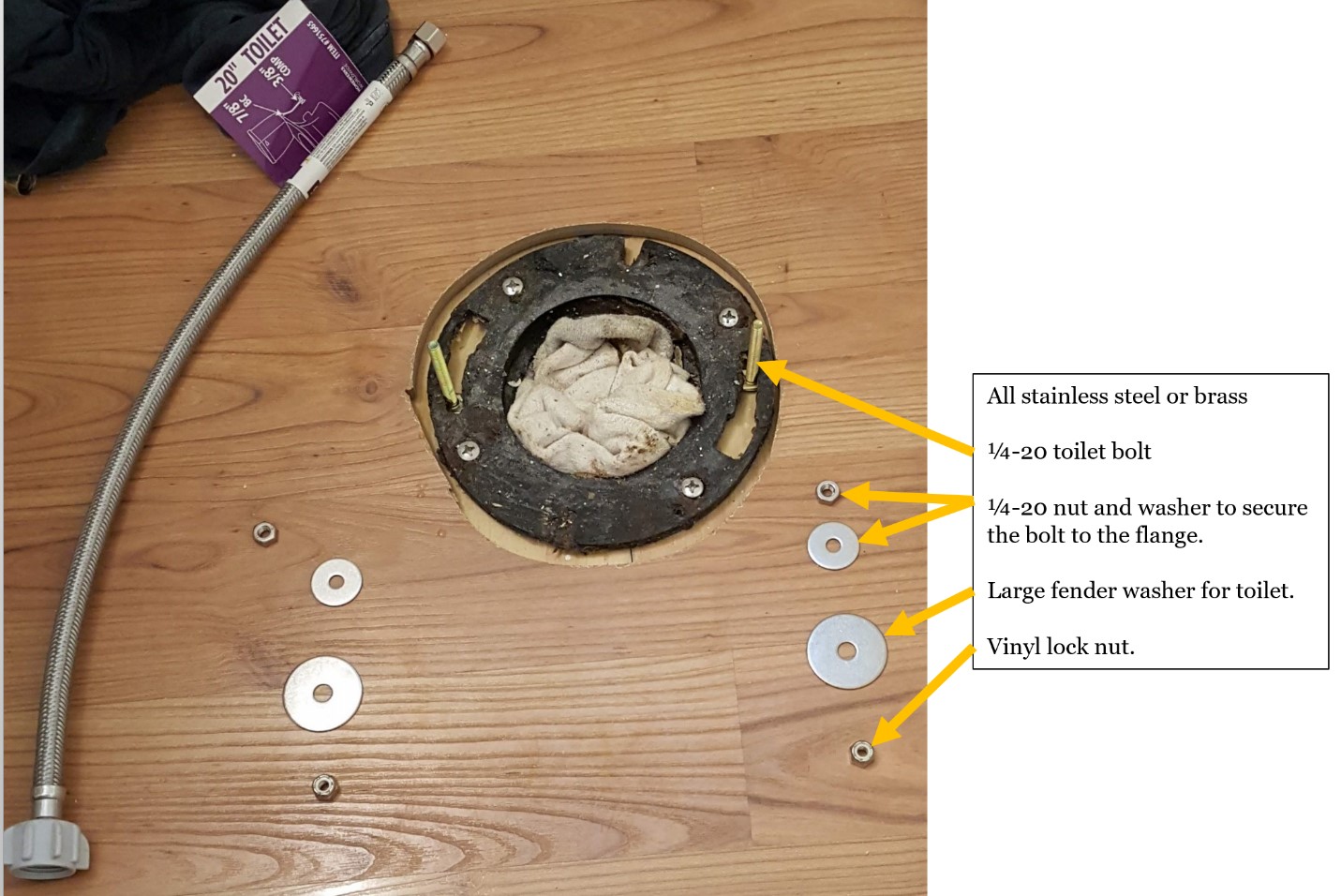

E1: Toilet Flange Hardware

E1: Toilet Siphoning

E2: Pedestal Sink

E2: Flat Space

E2: Cabinet Sink Gross

E2: Bathroom Sink Strainer Drain

E2: Vanity

E3: Shower Faucet

E3: Shower Valve

E3: Shower Head Piping

E4: Schluter Edging

Section F

F1: Kitchen Sink

F3: Kitchen Shelving

F4: Tile Tired

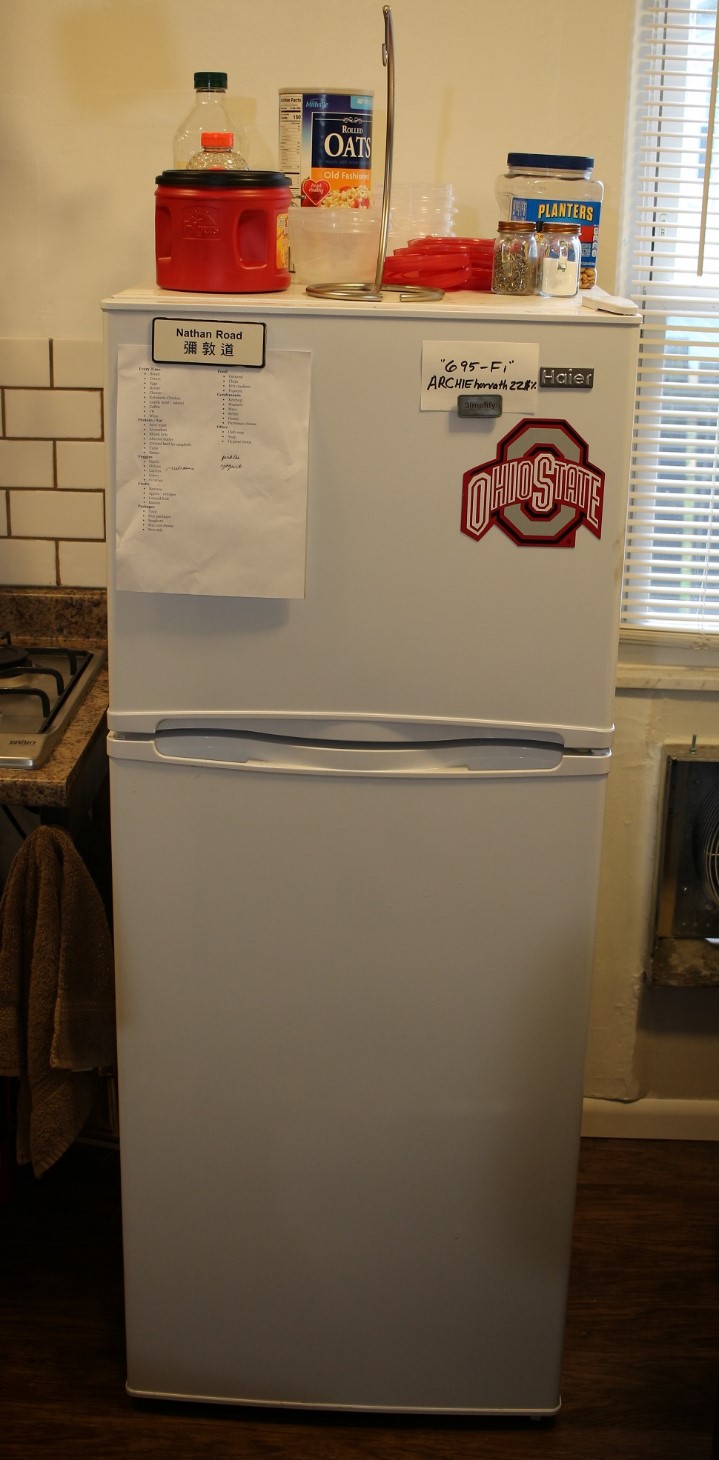

F5: Refrigerator

F6: Stove Top

Section G

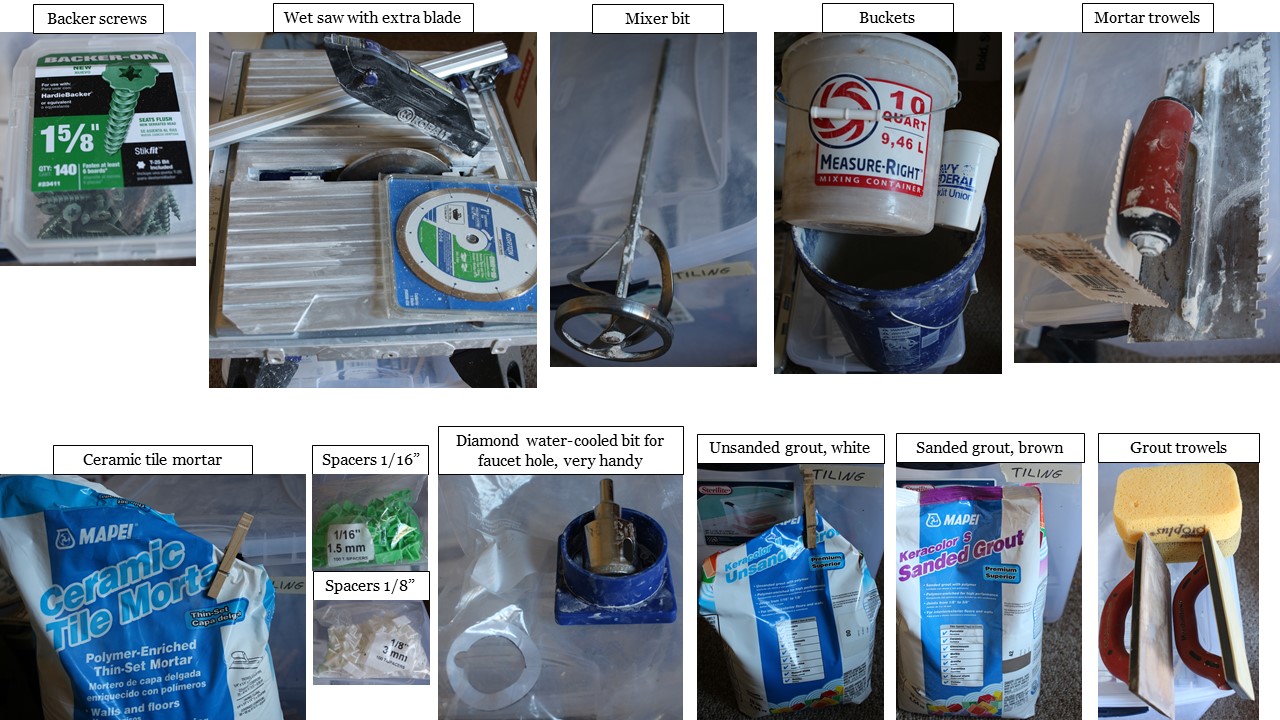

G1: Tile Kit

G1: Multi-Tool Etc.

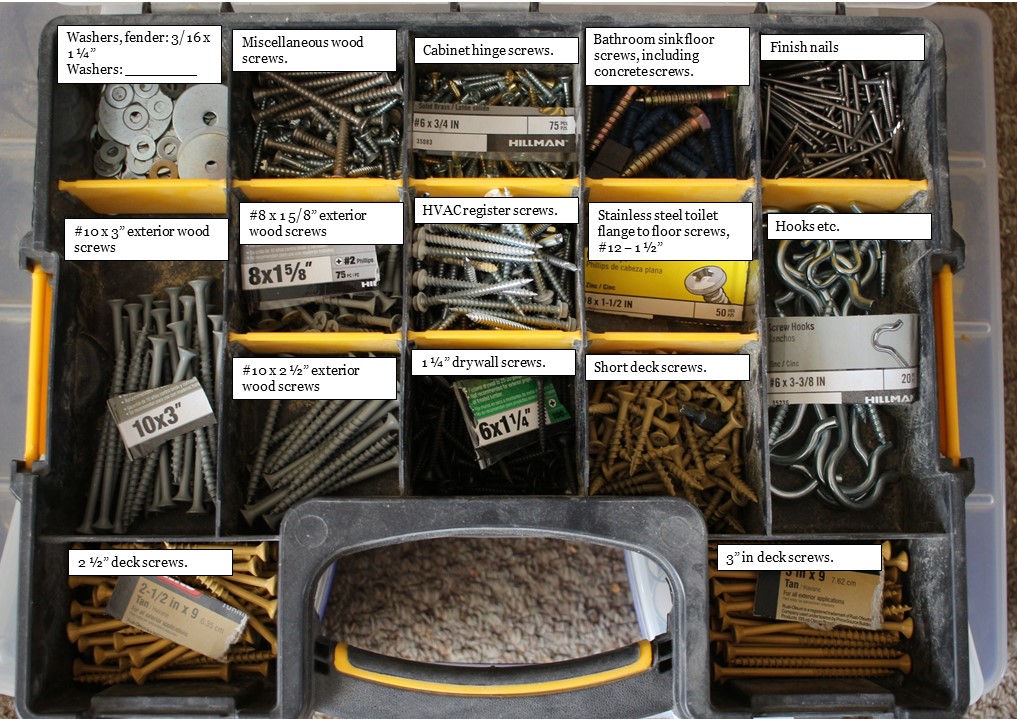

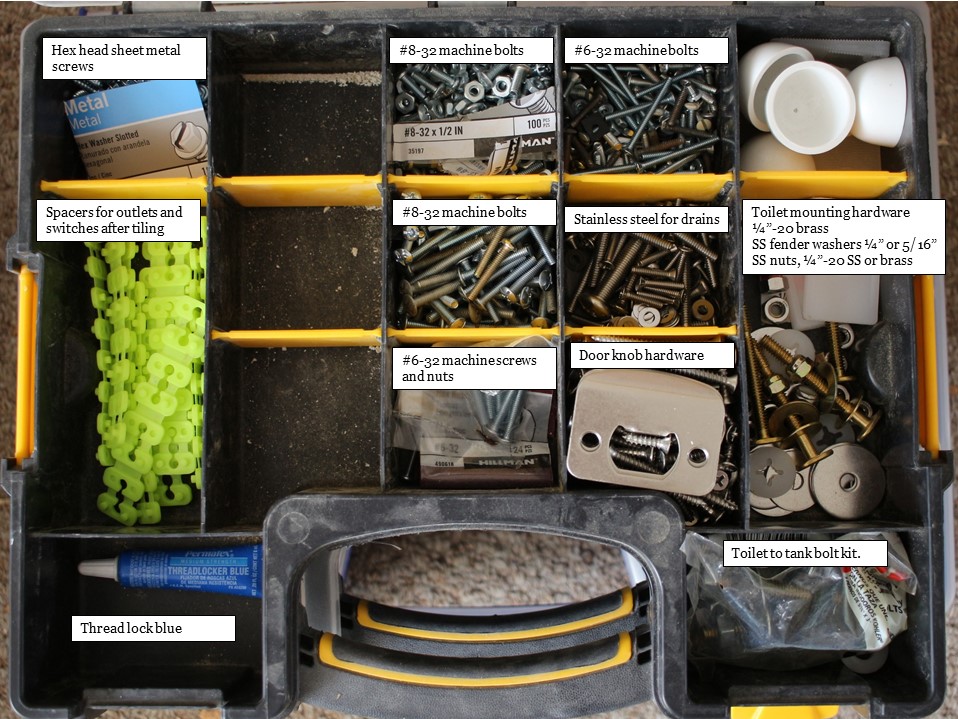

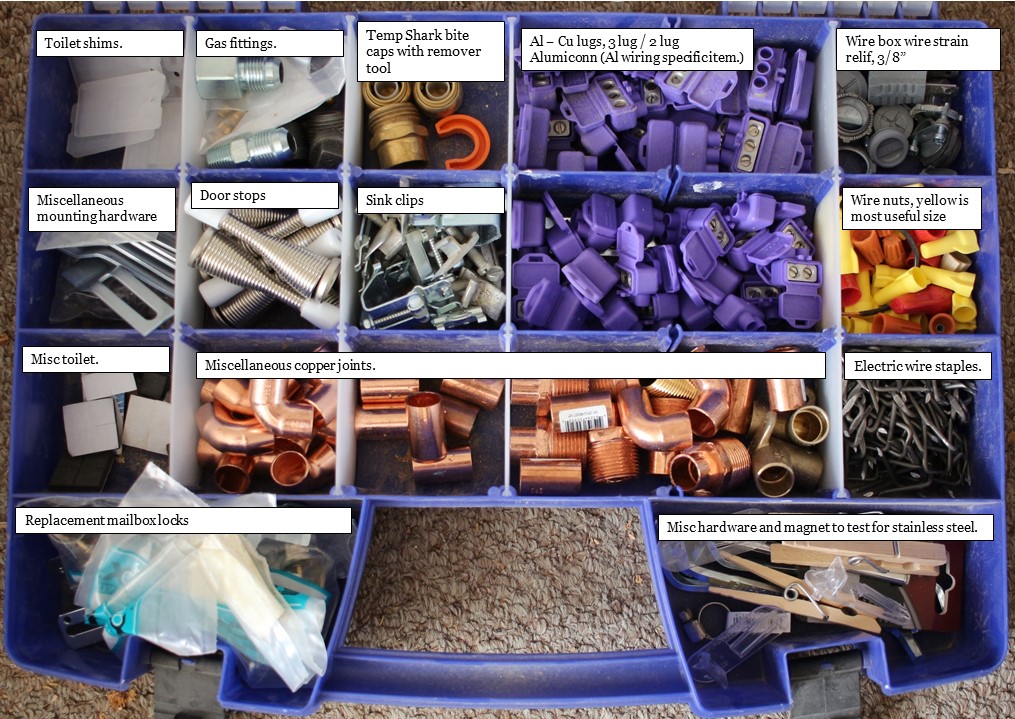

G2: Hardware Inventory

Shades of “Cash” Offers

There are two main aspects to every offer. The first aspect is the offer amount (=money from buyer). The second aspect is the “strength” of the offer.

Offer Amount

This is very straightforward. No matter how the buyer comes up with the money, the title company will receive the agreed upon purchase price from the buyer / lender / salty loan shark, and distribute the money to all the people to whom the seller owes money in relation to the property and transaction, then the remaining money to the seller. For the amount, it does not matter where the money comes from, it is all the same money to the seller at closing: dollars $$$.

The amount that reaches the seller depends on the seller’s situation, and can be estimated with a Net to Seller, example here. It does not depend on the source of the buyer’s money nor what the money is labeled within the offer.

The only way that an offer of the same purchase price can yield less or more to the seller is if there is another specific amount written on the contract that obligates the seller or buyer to pay something at closing. The most common example of this is, for example:

“Seller to contribute $2000 toward buyer’s closing costs and related fees.”

Let’s compare two offers.

Offer A: $150,000 / $2,000 in closing costs.

Offer B: $148,000 / $0 in closing costs.

Offers A and B are equal in amount because in offer A – though higher than offer B – the title company will distribute $2,000 from the seller’s funds to the buyer at closing. Offer A might be slightly more attractive to the buyer because the buyer brings less cash at closing because of the money being “kicked back” by the seller. To the seller, these offers are essentially the exact same.

Other common examples are when the seller pays for a warranty on the house, usually $500-$600 to a warranty company, or perhaps the seller agrees during the remedy period to pay for some defect that was found on the inspection.

Offer Strength, The Cash Continuum

“Cash is king,” so cash can get you good deals! … This is true, but there are many factors that influence a seller’s decision of whether to accept an offer or not, or which offer to accept if there are multiple. From strongest to weakest, here are the types of offers that a seller can receive, why they are strong / not as strong, and also which types of sellers consider which aspects of offers. Imagine you are the seller in this case and you are receiving multiple offers of the same amount, but with different strength factors:

Strongest

Cash, “As-Is,” No Inspection

This means that the buyer accepts the house in its current condition. The seller need not so much as set foot on the property again, only give the buyer agreed amount of time to arrange his funds (1-3 weeks usually), schedule a closing, then sign the deed to the buyer and receive the money.

Sellers who care: this matters most to a seller who is selling a house for which most banks won’t issue a loan. For example, when floors are not installed (sub-floor exposed), banks often will not lend even if the house would clearly be very valuable with just $2,000 worth of carpet installed. Complete rehabs want cash buyers because they don’t want to wait for the buyer to convince a construction lender’s slow bureaucracy to finance his project.

Sellers who don’t really care: cash is always strong, but for example when a seller is selling a house that is almost brand new, built by a reputable builder in a neighborhood where 3 similar houses have sold recently after passing inspections for near the offered price, the seller doesn’t really care where the money comes from. A cash buyer might be able to close faster, but it is only a difference of a few weeks at most.

Strong

Conventional Financing

This means that the buyer has been pre-approved for a standard loan. Most banks can close within 30 days, and require an appraisal. The appraisal is the primary risk to the seller, and the seller might also care about time to close. Sellers usually prefer banks that specialize in mortgages as opposed to “big banks,” but on a normal deal, either bank will close within 45 days at the most, and usually within 30 days.

“The Cash Continuum”

As we progress down this list, the buyer is bringing less and less of his own cash to the table. More cash is a stronger offer, so sellers are more likely to accept, and also as a general rule, the more cash you bring, the better deal you get from the lender. Most people know about the cut-off at 20% down, where the lender does not require the buyer to purchase Private Mortgage Insurance (PMI), but 20% down is just one of several levels. 10% down gets a slightly better deal than 5% down. “No money down!” loans exist, but they are expensive like credit card loans. There are deals above 20% as well. Banks will often give slightly lower rates to buyers who can bring 30% or 40% down. Most people don’t even consider purchasing with cash only, but still the more of your own cash you bring, the less risk the lender is taking, and the better deal you get.

Not as Strong

FHA Financing

This means that the buyer is getting a loan with help from the Federal Housing Administration. The FHA is a government entity and has inspection requirements and bureaucratic paperwork to complete. These often take more than 30 days, carry risk to the seller, and require more work from both parties to complete. FHA loans are therefore less attractive to sellers and considered weaker offers.

Contingent on the Sale of …

This means that the buyer can only complete the contract and purchase the house if the buyer sells his house first. Agents often advise sellers to turn down these offers (while encouraging the prospective buyer’s interest as much as possible), and remain on the market. However, sometimes sellers will take the chance and accept such an offer for an attractive price (this means it costs the buyer money).

Another option for the seller is to include an “Escape Clause” in the contract that says the seller still has the option to escape from a contract and accept another offer if a second buyer comes along while the first buyer tries to close the sale of his house. Click here for an explanation of the types of contract contingencies / MLS status.

Shades of “In Contract”

This is the continuum of how “in contract” a house it.

Imagine you are a buyer looking at houses and you want to know how available a house is based on its “MLS status.” In order from most available to least available, here they are:

Most Available

Active

- The seller advertises that he will sell for the listed price. Make an offer!

Back on the Market

- Same status as active, but the house was previously in a contract that fell through for some reason.

Active* …

*But Listed Very Low

- When the list price is clearly below market value, it has only been on the market a few days, and it is a hot sellers’ market, there could very well be multiple offers arriving to the seller, and the house will go to the highest strong offer. These usually close for near market value rather than the advertised lower price, or “over list price.”

Contingent Escape

- This means that the seller has a buyer who intends to purchase, but the seller demanded that the contract include an “escape clause” that he can “escape” from the contract if he chooses, i.e. something better came along.

- The most common reason for a Contingent Escape status is that the seller received an offer from “buyer 1” that was contingent on the sale of another house. Rather than deny the offer, the seller gives buyer 1 a chance to perform, motivating buyer 1. However, knowing that such an offer can take a long time and be very fickle, the seller wants to have the option to take a stronger offer if buyer 2 comes along to swoop the house up.

- When I want to search for just houses that are truly available, I do include Contingent Escape. These are not common, and it is better to be buyer 1, but they are likely to be available if you really want them.

- When Contingent Escape, you are buyer 2, and you have to contend with buyer 1, but the seller is not obligated to sell to buyer 1. The seller can choose your offer if he decides that it is better.

Probably not Available

“Contingent on Finance and Inspection”

- “Contingent on Finance,” and “Contingent on Inspection” do not exist separately as options on the MLS when the listing real estate agent enters status data. Therefore, when you see “Contingent on Finance and Inspection,” the seller has accepted an offer from a buyer, but the contract is still contingent on both or just one of these, finance or inspection. You do not know which without calling to ask. The agent / seller are not obligated to disclose the details of the contract.

- The seller must sell if the buyer performs.

Contingent on Inspection

- This means that the seller has a buyer, but the buyer has not yet completed the inspection portion of the due diligence. The inspection is probably the most common reason that a house returns to the market, but still is fairly rare. Either the inspector finds something unexpected that is wrong with the house, or finds something that that particular buyer will not accept.

- When this falls through: the house is in contract, and the buyer orders the inspection. The inspector lifts up insulation that covered the basement wall and sees large cracks in the concrete blocks, indicating that the foundation is shifting. The buyer is now looking at a house with a major problem that affects the sale value and the buyer’s overall interest. The seller will now probably have to go back on the market, and now officially knows about the cracks and is legally obligated to disclose the cracks to all future buyers.

- The seller must sell if the buyer performs.

Contingent on Finance

- This means that the seller has a buyer, but the buyer needs a loan and does not yet have a loan commitment. The deal is very likely to close, but there is a chance that the appraisal will be low, or the bank may do an inspection and decline to lend on the house.

- When this falls through: if the appraisal comes back below the contract price, often the buyer asks the seller to drop the price. The seller can then decline and go back on the market, accept the lower price, or demand that the buyer bring cash to cover the difference over the appraisal. The buyer is not required to brign cash unless that was written into the contract. These usually close, but in hot markets where buyers go over market value to get a house into contract, these deals fall through sometimes.

- The seller must sell if the buyer performs.

Pretty Much Sold

Pending

- This most often means that the seller has accepted a cash offer, no inspection, and is only waiting for the scheduled date at the title company or lawyer’s office to close the deal.

- When a bank / loan is involved, once a contract has progressed through the inspection and remedy period, the appraisal is complete and sufficient, and the bank has issued a loan commitment (commitment is much more than a “pre-approval”) the status becomes pending. In the most common transactions involving banks and loans, the loan commitment is not issued until just a few days before closing, so the listing agent never changes the status to pending just for a few days. These go directly from “Contingent on Finance and Inspection” to “Closed.”

- The seller must sell if the buyer performs, and the buyer is finished with due diligence. Pending houses are pretty much sold.

Not for Sale

- What it means: You can make an offer on a house that’s not for sale, but of course you have to offer enough to make the owner want to move unexpectedly.

- What you have to do to buy it: you approach the owner personally or through an agent and make an offer. The owner has to accept the offer.

- Cool story: I heard of a couple in Washington DC who lived in a townhouse worth ~$800,000. They lived in the townhouse because they had sold their house in a nearby neighborhood that was worth ~$1.5 million. It was not for sale, but sold like this. They were eating dinner one evening and they heard a knock at the door. There was a Chinese couple at the door who asked to look around the house they’d like to buy it. The owners said, “Uh, OK, why don’t you come back tomorrow at x time.” The Chinese couple returned the next day, looked around and said, “We would like to buy it ‘as-is,’ with the paintings on the wall, furniture, everything, all included, how much?” The owners consulted with a real estate agent and a lawyer, and asked for $2.5 million. The Chinese couple agreed. Sold! for an extra $ 1 million. The Chinese couple’s daughter was attending a nearby university and they wanted a place to stay while they visited.

- There are also companies that make offers on houses not for sale from distressed owners. “Cash for your house!”

Real Estate Summary, November 2018

Lawrence Yun is the chief economist for the National Association of Realtors®. He is very straightforward and he applies numbers to what everybody is feeling in the real estate market. This 10 minute interview covers what most people are talking about: a “slow-down” in real estate, rising interest rates, new home building, consumer preferences, etc.

Ventures Update September 2018

695 Riverview Drive

I have been renovating apartments consistently since May. The rent is paying for the renovations and the apartments keep getting better and better as I develop my system.

There is one empty right now with a waiting list for when I finish it.

Click here for the building’s website.

Writing Landlord Book!

Together with my neighbor landlord who has 40 years of experience with 40+ units, I am writing a book. For a title, I am thinking:

The Real Estate Reality Book: How to Make 10s to 100s of Thousands of Dollars Doing Actual Work, Creating Actual Value as a Real Estate Investor

Chapters:

- What is a Landlord Really? A Short History and the Modern Landlord

- Should I Even Do This? Guiding Principles for Your First Purchase, and Property Evaluation Spreadsheets

- Do It Right. Pride of Ownership and Money Come Hand in Hand

- Do It Myself, or Hire It? The “Money Flow Chart” Decision Tree

- The Numbers. Quantitative Analysis of Owning Real Estate

- Just Pick a Number and Use It. The “GRM Continuum”

- Operator’s Manual: Which [_____]I Buy and Why

- Operator’s Manual: Tools Required

- Operator’s Manual: Spreadsheet by Unit

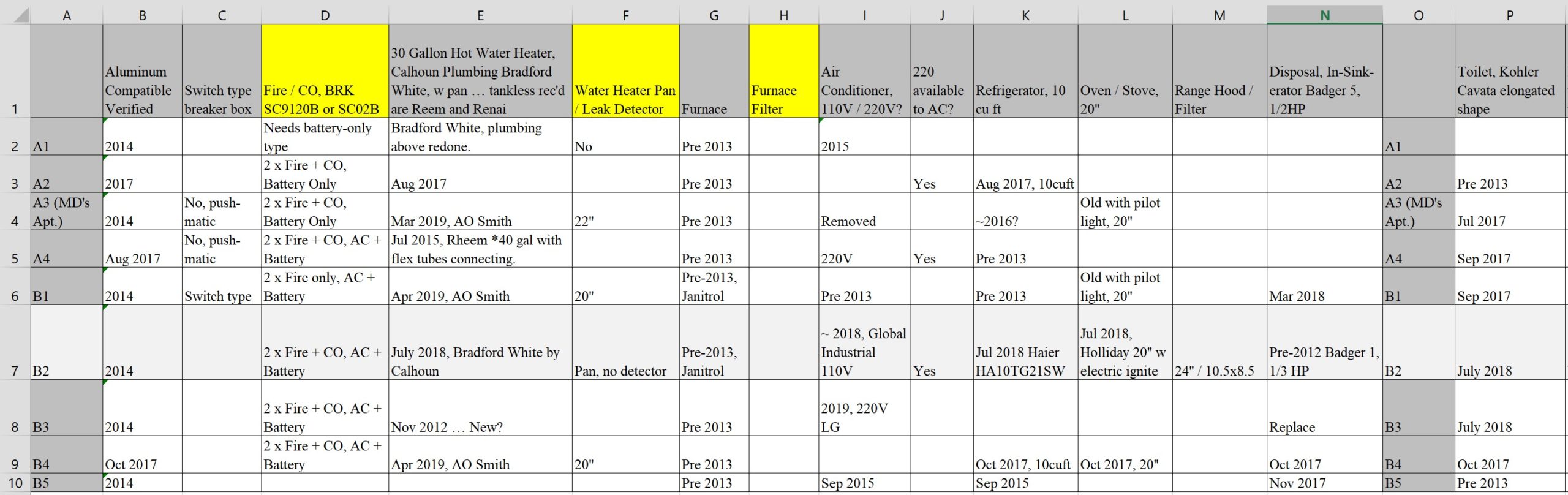

- Operator’s Manual: Dimensions Reference

- (Almost) Passive: Hiring a Property Manager

Real Estate Agent

I am selling my parents’ house:

I also made a video for another agent on his listing just like that. It came out great, and I’m looking to do more of them for a fee.

Nate TV

The What to Watch series got too much too handle weekly and I covered too many subjects to effectively get people involved.

I am starting the very specific channel, Nate the Columbus Commuter Biker

Kineomen

The venture capital thing is challenging. I am getting with my brother to make a list of lessons learned as we go forward in this type of pursuit. Kineomen is alive and well.

Simple Kneads Gluten-Free Bread

Simple Kneads is consistently producing its quality product and growing as a brand.

Vino de Coco

I still plan to visit the Philippines. Still.

Real Estate Summary, July 2018

Average Sale Price

- $238,655, Jul 2018, 4.9% increase 1-yr, 37.2% increase 10-yr

- $227,572, Jul 2017

- $173,940, Jul 2008

The year-over-year increase in price for July 2018 compared with the YoY increase in July 2017 is less, so the increase has slowed. The YoY increase in July 2017 was 6.4%. From the MLS chart, the last time that the price increase was this slow was late 2014, so it appears by that measure the market has cooled off a bit, or is just a bit less hot. The price still increased don’t forget. That is good. The last time there was an overall YoY price decrease was 2011.

Source: http://www.columbusrealtors.com/stats/

Months Supply of Inventory

- 1.9 months, Jul 2018

- 11.2 months, Jul 2010 – highest for July in last 10 years.

- 2.0 months, Jul 2017 – last year’s hot market

We are still in a historical seller’s market.

Source: http://www.columbusrealtors.com/stats/archives.aspx

Interest Rate, 30 Year Fixed-Rate Mortgage

- 4.54%, 6 Sep 2018, most recent

- 4.46%, 8 Mar 2018

- 3.95%, 4 Jan 2018

- 3.41%, 7 Jul 2016, 5-year low

- 6.04%, 20 Nov 2008, the last time rate was over 6%

How much has the 30-year fixed rate gone up? It increased above 4% in January this year, reached 4.46% by March, and has held steady since then. The five year low was 3.41% in July 2016. Check out this interactive chart from Freddie Mac:

http://www.freddiemac.com/pmms/

What To Do, Sellers

Hold tight. The demand is still there.

What To Do, Investors

- Do: Improve / develop what you already own, and get it performing.

- Do: take opportunity to start as a wholesaler / real estate agent / manager.

- Don’t: buy on a variable rate loan.